Abstract

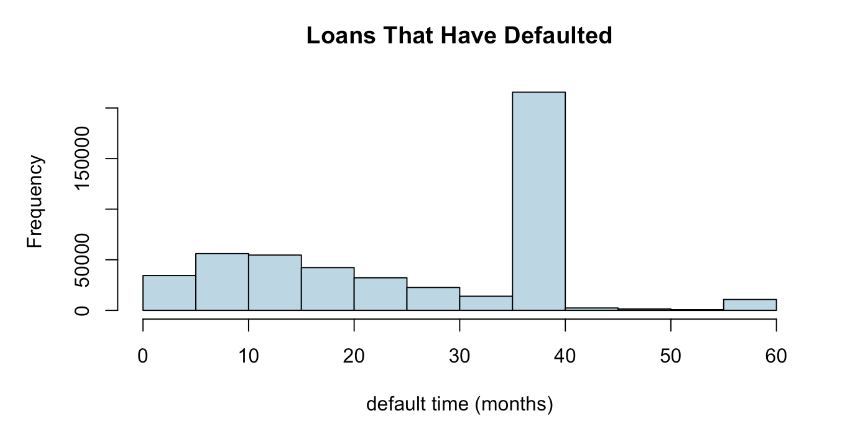

This paper explores the use of copula models for analysing competing financial risks, with a particular focus on modelling the dependence between loan prepayment and default events. Beginning with a theoretical overview of copula functions and their application within a competing risks framework, we evaluate the performance of different copula families through simulation studies. These simulations demonstrate that copula-based models can effectively recover both marginal and dependence parameters. The methodology is then applied to a real-world dataset of over two million loans from the Lending Club. Marginal distributions are selected using AIC criteria, with a Weibull distribution fitted for prepayment times and a three-component Weibull mixture for defaults, due to evident multimodality. The results highlight the value of flexible marginal modelling and copula-based approaches in capturing complex interdependencies between financial risks.

View the pdf in another tab here